The critical role data plays in helping Asia Pacific SMBs combat fraud

Data has become a crucial ally in the fight against fraud in an increasingly digital Asia Pacific. Small and medium-sized businesses (SMBs) are navigating a landscape teeming with sophisticated fraudsters armed with advanced tools. In this high-stakes environment, harnessing data becomes critical for SMBs to scale security and fight fraud.

Real-time payments (RTP) and Buy Now Pay Later (BNPL) are among the fastest-growing payment methods in the region, along with digital wallets, debit transfers, and mobile payments.¹ However, despite their widespread acceptance, these payment methods, particularly card and digital wallet payments, can be often perceived to have higher fraud rates.² The complexity of fraud techniques is also rising, and many SMBs find themselves ill-equipped to counter these threats effectively.

Fortunately, the surge in digital transactions has a silver lining. It provides SMBs with a treasure trove of data that can potentially help them in their fight against fraud.

Data’s potential as a weapon against fraud

Across the Asia Pacific region, SMBs are already leveraging this expanding repository of data to make better business decisions. According to IDC, 40 per cent of medium-sized businesses in the region will increase their investments in analytics by 2027, aiming to make sense of the consumer data they collect and use it to improve business outcomes.³ The data gathered from various digital transactions offers SMBs a comprehensive overview of consumer behaviour, spending patterns, and market trends.

Similarly, this data can be utilised to strengthen fraud prevention and security measures. SMBs, financial institutions, and governments can harness the power of data to safeguard transactions. By analysing payment data, these organisations can identify patterns and anomalies indicative of fraudulent activity. For instance, unusual spending behaviours, atypical transaction locations, or spikes in transaction volumes can be flagged for further investigation.

Additionally, sharing information about the latest fraud trends and tactics is critical to helping SMBs win the fight. This collaborative approach helps the entire ecosystem stay updated on the latest risks. For example, when a new type of fraud scheme is detected, sharing details about its characteristics and methods can enable SMBs to recognise and defend against similar attacks. This collective intelligence significantly enhances the ability to prevent and respond to fraud across the board.

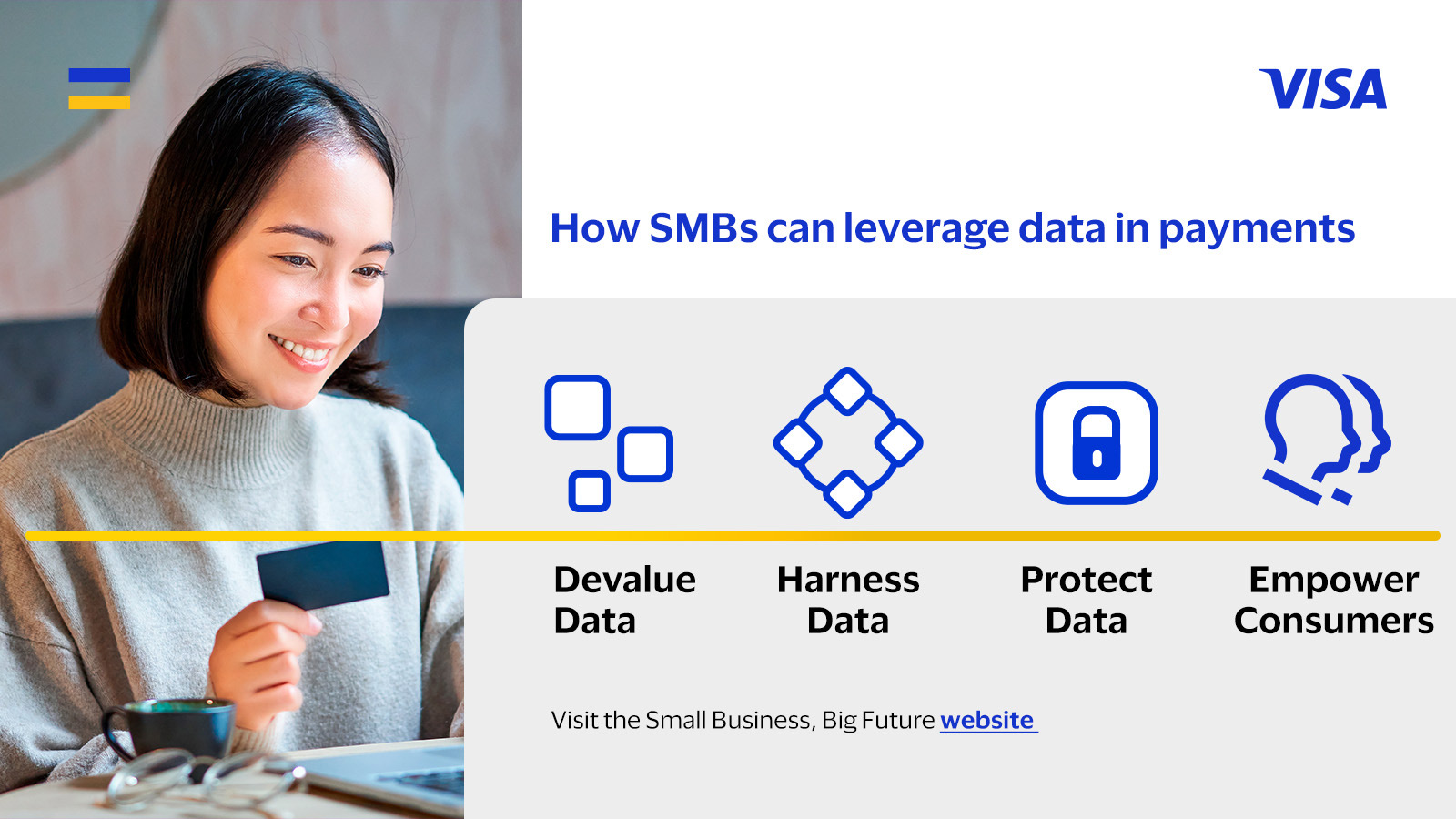

Four strategies to make data an ally

To elevate payment security, SMBs and the broader payments ecosystem can leverage four main strategies to address evolving fraud by protecting and leveraging data:

1. Devalue data to mitigate risk

One effective method to protect sensitive information is replacing it with non-sensitive equivalents, such as tokens, which are useless to fraudsters if intercepted. Tokenisation technologies enhance transaction security and ensure compliance with data protection regulations, such as the Payment Card Industry Data Security Standard (PCI DSS). By devaluing data, businesses can significantly reduce the risk and impact of data breaches, ensuring that even if data is intercepted, it cannot be misused by fraudsters.

2. Harness data to get ahead of fraud

AI-powered data analytics can provide a real-time risk score to help identify good and bad transactions. By leveraging insights with the help of organisations like issuers, SMBs can manage high-risk purchases and suspicious activity. Examples of such solutions include Visa Advanced Authorisation and Visa Risk Manager, which help detect and prevent fraudulent transactions with the support of AI-driven risk scoring and management.⁴ Harnessing data also allows for the continuous refinement of fraud detection algorithms, improving their accuracy and effectiveness over time as they learn from new patterns and behaviours.

3. Protect data for robust security

SMBs must utilise mechanisms, tools, and systems to protect consumer data. This includes employing encryption for data at rest and in transit, implementing strict access controls to safeguard sensitive information, and performing regular security audits. Visa’s investments in utilising technologies and standards, like the Secure Credential Framework, Digital Authentication Frameworks, and EMV 3-D Secure, exemplify such protective measures.⁵ Additionally, businesses should stay updated with the latest security protocols and industry best practices to maintain a robust defence against emerging threats.

4. Empower consumers for additional defence

Educating consumers on secure online practices and recognising fraudulent schemes is crucial. Awareness campaigns, real-time fraud alerts, and educational resources can help consumers protect themselves against potential fraud. When consumers are well-informed, they can act as an additional line of defence, promptly reporting suspicious activities and taking proactive steps to safeguard their own financial information.

Safeguarding SMB payments with data as a shield

As the digital economy in Asia Pacific continues to grow, SMBs must use data strategically to combat fraud and enhance security, thereby protecting both their operations and consumers. Implementing data security practices such as tokenisation, real-time analytics, and robust encryption is crucial for SMBs to protect their transactions and data and stay ahead of fraudsters.

Moreover, SMBs, financial institutions, and governments must intensify their efforts in fraud prevention and consumer education to strengthen the region's digital transaction security. By adopting these measures, SMBs can effectively turn data into a formidable weapon against fraud, ensuring a safer digital environment for everyone involved.

¹ Visa, Enhancing Small and Medium-Sized Business (SMB) Financial Security and Fraud Prevention, 2024

² Visa, Enhancing Small and Medium-Sized Business (SMB) Financial Security and Fraud Prevention, 2024

⁴ Visa, Visa Advanced Authorisation and Visa Risk Manager, accessed May 2024

⁵ DigitalCFO Asia, Visa launches payment security initiatives in Singapore to combat rising fraud, 2023